Washington, D.C. (Oct. 8, 2025)

In a significant policy shift, the U.S. Department of the Treasury and the Internal Revenue Service (IRS) have jointly announced that certain penalties assessed in 2025 may be waived under long-standing relief programs. The move is intended to ease the burden on taxpayers struggling to keep pace with deadlines and evolving rules.

Background & Context

While the IRS has long maintained penalty-relief mechanisms (such as First Time Penalty Abatement and reasonable cause waivers), the new announcement underscores the Treasury’s backing and clarifies application during the current tax year. Get Tax Relief Now+3IRS+3IRS+3

The relief applies to penalties tied to failure to file, failure to pay, and failure to deposit in many cases, though not all penalties are eligible. IRS+2IRS+2 The IRS will continue to evaluate requests through existing processes, rather than issuing blanket waivers to all taxpayers.

What the Agencies Say

Treasury and IRS officials emphasized that this is not a “free pass” but rather a reaffirmation of options already in place—now with clearer signaling and administrative support.

An IRS spokesperson said,

“In 2025, we are reinforcing our commitment to helping taxpayers by ensuring eligible penalty relief is more accessible under current provisions.”

From the Treasury side, a senior official added,

“This step complements broader IRS modernization efforts and aims to reduce uncertainty for taxpayers who otherwise qualify under historic relief policies.”

What Is Confirmed vs. What Remains Unclear

Confirmed:

The relief will operate within the framework of administrative waivers already codified by IRS policy. IRS+1

Eligible penalties include late‐file, late‐pay, and deposit penalties. IRS+1

Taxpayers must still apply (often via phone or in writing, e.g., Form 843) to have penalties waived. IRS+2IRS+2

Relief may include interest reduction tied to removed penalties. IRS+1

Unclear or Conditional:

The announcement does not guarantee automatic waiver for all taxpayers.

Some penalties—such as fraud-based assessments or certain accuracy-related penalties—may remain ineligible. IRS+1

How aggressively the IRS will approve such relief under constrained agency resources is yet to be tested.

The timeline for processing relief requests under this renewed emphasis remains to be seen.

What Taxpayers Should Do Now

Review any IRS notices disclosing penalties—look for instructions on how to request relief.

If eligible (e.g. good compliance history, reasonable cause), submit a waiver request promptly via phone or Form 843. IRS+3IRS+3IRS+3

If denied, taxpayers may appeal or provide additional documentation supporting mitigating circumstances. IRS+1

Stay vigilant of IRS updates, as further guidance or formal rules may be forthcoming.

Next Steps & Outlook

Observers note that this announcement may spur more waiver requests and put pressure on IRS staffing and adjudication resources. Tax professionals say the key will be consistent, transparent adjudication.

Legislatively, Congress may watch whether relief is efficiently handled or abused. Meanwhile, many taxpayers—especially those who missed filing or payment deadlines—may view the move as welcome breathing room.

If the IRS and Treasury follow through and process relief expeditiously, this could mark a milestone in shifting tax enforcement toward more flexible, taxpayer-friendly regulatory practice.

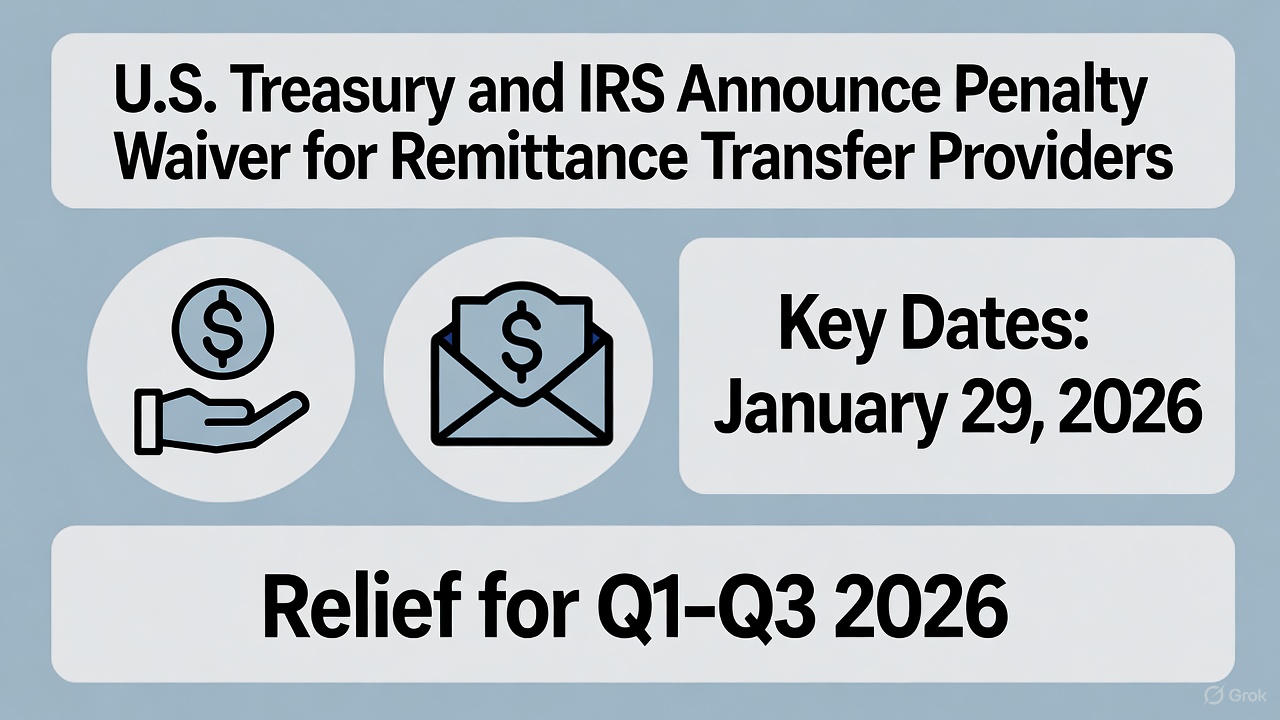

### IRS Relief for Remittance Transfer Providers: Penalty Waiver Announcement

On October 7, 2025, the U.S. Department of the Treasury and the Internal Revenue Service (IRS) announced targeted penalty relief for remittance transfer providers in response to a new excise tax introduced under the "One, Big, Beautiful Bill" (OBBB). This measure, detailed in IRS Notice 2025-55 and IR-2025-102, waives deposit penalties for failures occurring in the first three quarters of 2026 (January through September). The relief aims to ease the transition for providers as they implement systems to collect and deposit the 1% excise tax on certain outbound remittance transfers, which takes effect in 2026.

#### Key Details of the Announcement

- **What It Covers**: Automatic waiver of penalties for late or insufficient deposits of the remittance excise tax. The first semi-monthly deposit is due January 29, 2026.

- **Who Qualifies**: Remittance transfer providers (e.g., companies handling international money transfers). This does not provide direct payments or rebates to individual senders; however, providers may pass the tax cost to customers.

- **Why It Matters**: The OBBB imposes the new tax to generate revenue, but Treasury and IRS recognized potential implementation challenges, such as updating software and processes, making this relief a practical adjustment for sound tax administration.

- **No Action Required for Relief**: Eligible providers receive the waiver automatically if they meet the criteria—no separate application needed.

- **Related Forms**: Providers will report and deposit via Form 720 (Quarterly Federal Excise Tax Return).

This is not a broad "relief payment" program like stimulus checks; instead, it's a targeted waiver to avoid punitive fines during the rollout. For full guidance, refer to the official IRS notice.

#### Summary Table: Timeline and Impact

Aspect Details

------------------------- ----------------------------------------------------------

**Announcement Date** October 7, 2025

**Effective Period** Q1–Q3 2026 (Jan 1–Sep 30, 2026)

**Tax Rate** 1% on certain remittance transfers

**First Deposit Due** January 29, 2026 (semi-monthly schedule)

**Beneficiaries** Remittance providers only (not individuals)

**Source Document** IRS Notice 2025-55 and IR-2025-102 |

Comments

No comments yet. Be the first to comment!